In the high-velocity banking landscape, the distance between a loyal customer and a lost account is measured in milliseconds. As financial services move toward an agentic future, the primary touchpoint remains the oldest and most personal: the human voice.

For too long, the banking voice experience has been defined by the rigid, frustrating walls of legacy Interactive Voice Response (IVR). These systems, designed in an era of scarcity, were built to deflect customers rather than resolve their needs. Today, that friction is a terminal brand risk.

For a CXO in the BFSI sector, the tension is palpable: you must scale support exponentially while maintaining an airtight security posture and complying with the most stringent data protection laws in history.

This blog explores how the voice AI agent is not just replacing menus, but building a resolution-first engine that understands financial nuance, regional dialects, and the critical importance of trust in a digital-first economy.

The Banking Voice Crisis: Why IVR Is the Biggest Barrier to Trust

Traditional IVR systems were designed to protect the call center from the customer, not to serve the customer’s intent. In 2026, this deflection-first strategy is a catalyst for churn.

The zero-response fatigue in traditional banking

When a customer calls a bank, it is rarely for a casual check-in. They are calling because a transaction failed, a card is missing, or a life-altering loan is in the balance. In these high-anxiety moments, being met with a Press 1 for accounts, Press 2 for cards menu feels like an institutional dismissal. This zero-response fatigue occurs when the interface becomes a barrier to the solution.

RELATED: Why Enterprises are Replacing IVR with Voice Agents

Research shows that 70% of banking customers will abandon a call if the IVR exceeds three levels of depth. For modern banks, the cost of this fatigue isn’t just a dropped call; it is the erosion of the ‘primary bank’ status as customers migrate to agile fintechs that offer immediate, voice-first resolution.

The cost of security-induced friction

Security protocols are the bedrock of banking, but they often create a verification trap.

Customers find themselves repeating their date of birth, last four digits of their card, and mother’s maiden name across multiple departments. This friction-heavy KYC process adds significant Average Handle Time (AHT) and irritates the user before the actual problem is even addressed.

ALSO READ: How to Measure Voice AI ROI: The Framework for Enterprise CX Leaders

Voice AI for banking changes the equation. By integrating background voice biometrics and real-time OTP verification into the natural flow of the conversation, the AI verifies the customer’s identity while they are explaining their problem.

This simultaneous verification reduces friction, tightens security, and allows the human agent (if needed) to start the conversation with the identity already validated.

Why deflection is a failed strategy

For decades, call center managers were incentivized to increase IVR Deflection rates, which is the percentage of calls that never reached a human.

The goal was cost-saving.

However, deflection without resolution is a failure. If a customer hangs up because they are frustrated, they haven’t been deflected; they’ve been alienated. The North Star metric has shifted to Resolution at the Edge.

Voice AI agents are empowered to actually solve the query like hotlisting a card, increasing a credit limit, or rescheduling an EMI directly in the voice channel. This is an autonomous service that delivers true ROI.

Strategic Use Cases: Where Voice AI for Banking Drives Real-Time ROI

Voice AI has transitioned from a generic support tool to a surgical instrument used by specialized departments to drive revenue, recovery, and risk management.

High-speed fraud reporting and card hotlisting

In the event of a security breach, every second counts. If a customer notices a fraudulent transaction at 2:00 AM, waiting for a human agent to pick up the phone is unacceptable.

The Voice AI provides a 30-second fraud response path. The customer can call, authenticate via voice or WhatsApp-OTP, and hotlist their card in a single, fluid interaction. By the time a human agent would have finished their opening script, the AI has already secured the account and triggered a replacement card issuance.

ALSO READ: WhatsApp Voice Agents: The Enterprise Guide to Deploying on the World's Largest Messaging Platform

This speed doesn’t just prevent loss; it creates a hero moment for the brand that earns lifelong customer loyalty.

Automated loan eligibility and lead qualification

The outbound potential of Voice AI is often overlooked. Instead of having high-cost sales officers make cold calls to qualify leads, banks use Voice AI to conduct eligibility checks. The AI can reach out to 10,000 potential loan applicants in an hour, asking qualifying questions about income, existing debt, and funding requirements.

Only the leads that meet the bank’s criteria and express immediate interest are then transferred to a human loan officer. This increases sales velocity by 40% and ensures your human team spends 100% of their time on high-probability closures.

Debt collection and PTP negotiation

Debt recovery is one of the most sensitive areas in BFSI. Human collectors often face high stress, leading to inconsistent tones that can border on harassment. Voice AI, however, is 'professionally persistent.' It never gets tired or frustrated. It can call delinquent accounts in Bucket 1 (1-30 days) to offer polite reminders and, crucially, negotiate 'Promise-to-Pay' (PTP) dates.

Because customers often feel less 'shame' talking to an AI about financial distress, they are more likely to be honest about their repayment capacity, leading to higher recovery rates and more accurate cash flow forecasting for the bank.

Personalized wealth management and next-best action nudges

Voice AI can analyze a customer's spending patterns and call them with personalized financial advice.

For example, if a customer has a large idle balance in their savings account, the AI can call to suggest a high-yield Fixed Deposit or a Mutual Fund SIP.

This next-best action approach turns the call center into a profit center. By using a voice that sounds empathetic and authoritative, the bank can provide wealth management services to the mass-retail segment that was previously only available to high-net-worth individuals.

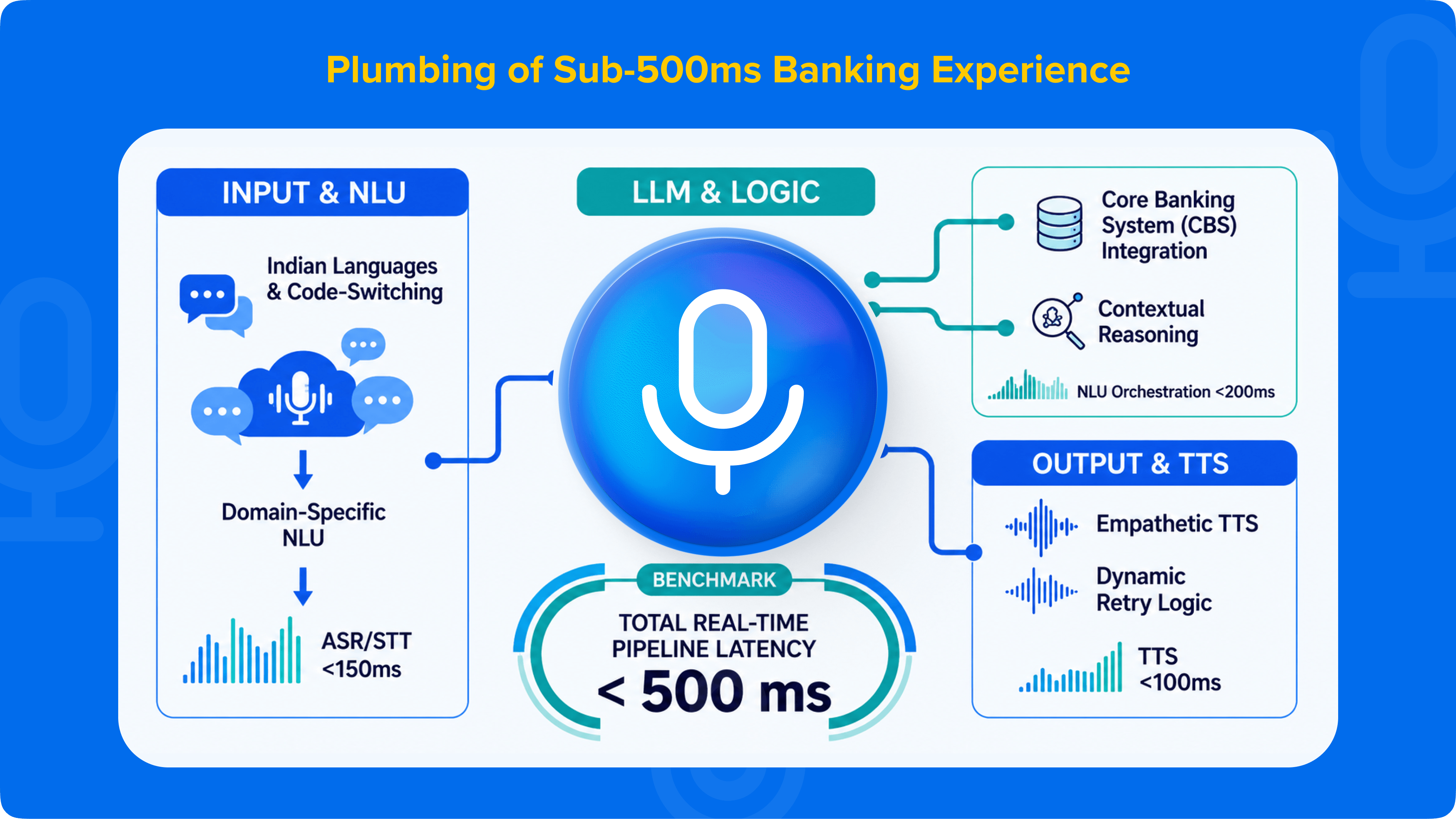

Technical Architecture: The Plumbing of a Sub-500ms Banking Experience

For a bank, the technology behind the voice is a matter of security and performance. Achieving a human-like conversation requires a specialized stack.

The ASR-LLM-TTS Pipeline: Optimizing for the Indian ear

The greatest challenge in Indian banking is the diversity of accents and dialects.

A standard global ASR (Automatic Speech Recognition) engine often fails to understand a customer from rural Karnataka or suburban Punjab.

ALSO READ: Voice Agents for Indian Languages: What Enterprise-Grade Really Means in 2026

Haptik’s engine is specifically tuned for Indian phonetic nuances. We optimize the pipeline from the moment the customer speaks to the moment the AI responds to stay under 500ms. This 'ultra-low latency' is essential; anything slower, and the customer will start talking over the AI, breaking the conversational flow.

Real-time API hooks into core banking systems

A Voice AI agent is only as smart as the data it can access. Haptik integrates natively with core banking systems allowing the AI to pull live balances, verify transaction history, and trigger internal workflows (like blocking a card) in real-time.

Without this deep integration, a voice agent is just a glorified FAQ bot. With it, it becomes an autonomous digital employee with the power to execute.

Handling code switching and Hinglish in high-stakes dialog

In India, most banking conversations are multilingual.

A customer might start in English and switch to Hindi when describing a problem: 'My card is blocked, please ise jaldi unblock kardo.'

A successful banking AI must handle this 'code-switching' natively. Haptik’s voice AI platform is built to process mixed-language inputs, ensuring that the intent is captured correctly regardless of the linguistic blend used by the customer.

Compliance, Security, and the RBI/DPDP Mandate

In 2026, compliance is the product. Every interaction must be an airtight demonstration of regulatory adherence.

ALSO READ: Voice Agents for BFSI: High-Compliance Conversations at Enterprise Scale

Solving for consent-first banking under the DPDP Act

The Digital Personal Data Protection (DPDP) Act mandates that banks have clear, specific, and revocable consent for using customer data.

Our Voice AI begins high-stakes interactions by capturing verbal consent, which is then timestamped and logged as an immutable record. This ensures the bank is always 'audit-ready' and provides customers with the transparency they demand in a post-privacy world.

Real-time PII redaction and voice encryption

During a call, a customer might say their card number or CVV. Haptik’s architecture features a 'Security Shield' that redacts this sensitive PII (Personally Identifiable Information) from all text transcriptions and audio logs in real-time.

We ensure that while the AI 'hears' the data to process the transaction, the data is never stored in a readable format, significantly reducing the bank's surface area for data breaches.

The Haptik Advantage for BFSI Voice AI

Haptik’s role in the banking sector is defined by our focus on outcomes, scale, and deep integration with the existing enterprise ecosystem.

Outcome-driven architecture: Moving beyond 'Talk Time' to PTPs

We don't measure our success by how long our AI talks, but by what it resolves.

For a bank, an outcome is a card unblocked, a loan lead qualified, or a payment promise (PTP) secured.

Our logic is entirely outcome-driven, meaning every conversational turn is designed to move the customer toward a resolution, reducing the need for costly human callbacks.

100+ OOTB integrations

The biggest barrier to AI adoption is integration. Haptik solves this with over 100 out-of-the-box (OOTB) connectors.

Whether your contact center runs on any modern tool, or your data sits in a legacy mainframe, we can plug in and go live in weeks. This allows banks to bypass the 'Build vs. Buy' trap and start seeing ROI immediately.

Meta Premier Partner: Bringing the bank to WhatsApp voice

As a Meta Premier Partner, Haptik is at the forefront of the WhatsApp-first banking revolution.

ALSO READ: WhatsApp Voice Agents: The Enterprise Guide to Deploying on the World's Largest Messaging Platform

We enable banks to offer voice-based services directly within WhatsApp, allowing customers to send voice notes or engage in voice calls on the platform they use every day. This omnichannel orchestration ensures that the banking experience is as seamless as a message to a friend.

Forward-deployed teams: Owning the post-go-live ROI

Haptik’s forward-deployed teams consist of domain specialists who work alongside your operations and IT teams.

We monitor performance, tune for regional dialects, and optimize recovery logic post-launch. We stay through the go-live and beyond, ensuring your recovery and resolution KPIs are met month after month.

Bottom Line

In the high-stakes world of BFSI, the voice channel is where brand trust is either solidified or shattered.

Transitioning from legacy IVR to agentic voice AI allows banks to solve for the verification trap, moving from five-minute menus to thirty-second fraud resolutions.

By embedding RBI-compliant security and regional dialect intelligence into every call, you move beyond simple deflection toward a model of autonomous service. In 2026, the most successful banks are those that view voice AI not as a support cost, but as a secure, high-velocity engine for customer experience.

FAQs

source on Google